GSTR-9 & GSTR-9C Compliance for FY 2024–25 📊🧾

Dec 31, 2025 • Sobiya Fatima • Discount Sales / Sale & Promotion

Source:

Hyderabad Deccan Chronicle

This document provides a detailed compliance overview for businesses required to file Annual GST Return (GSTR-9) and Reconciliation Statement (GSTR-9C) for the financial year ending 31 March 2025. It focuses on applicability, turnover thresholds, updated reporting formats, deadlines, and technical filing requirements.

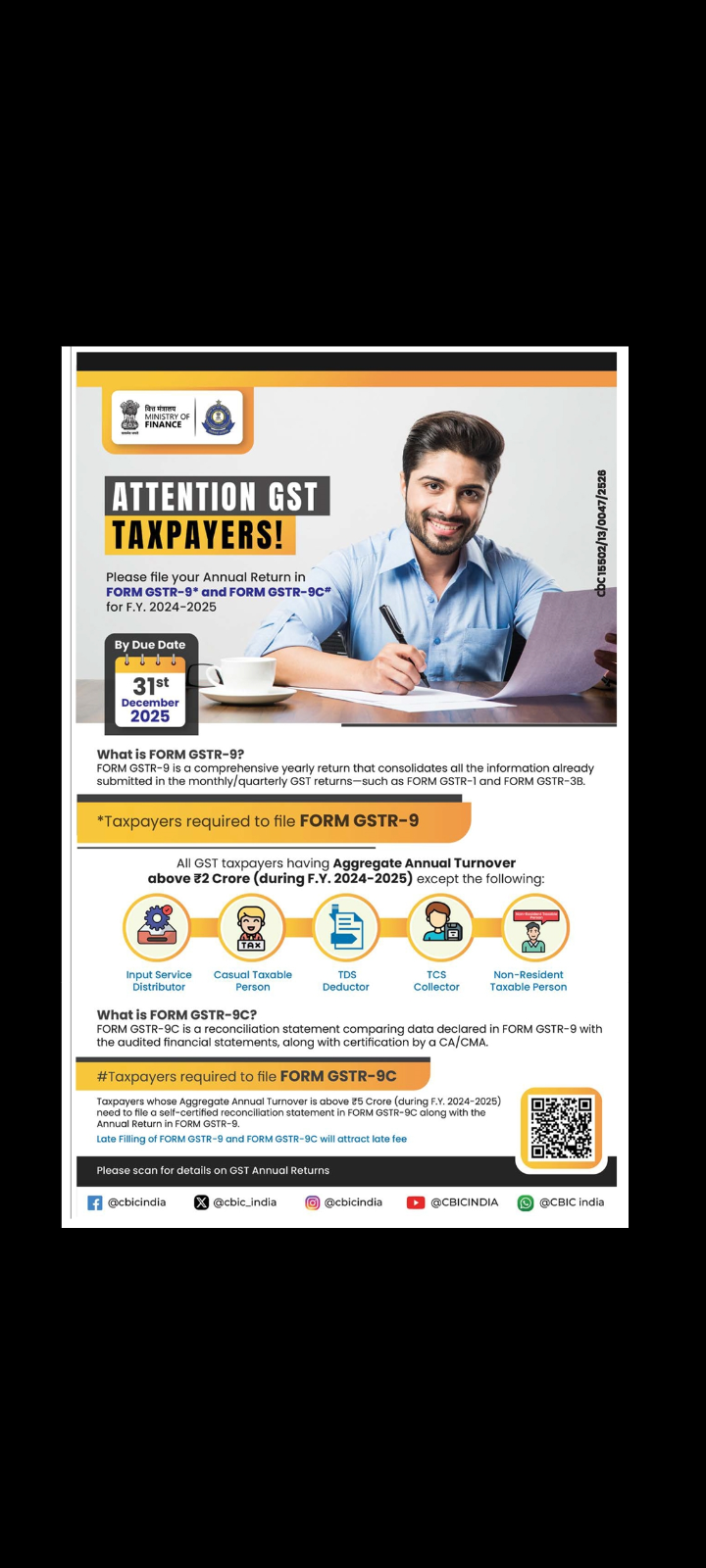

Applicability Based on Turnover 💼📈

Filing requirements are determined by a taxpayer’s aggregate annual turnover during FY 2024–25:

🟢 Turnover up to ₹2 Crore

GSTR-9 is not mandatory

Voluntary filing is permitted

🔵 Turnover exceeding ₹2 Crore

GSTR-9 filing is mandatory

🔴 Turnover exceeding ₹5 Crore

Both GSTR-9 and GSTR-9C are mandatory

Categories Fully Exempted from GSTR-9 🚫📑

Regardless of turnover, the following taxpayers are not required to file GSTR-9:

Composition dealers (they file GSTR-9A)

Casual taxable persons

Input Service Distributors (ISD)

Non-resident taxable persons

Statutory Due Date & Late Fee Provisions ⏰⚠️

📅 Due Date: 31 December 2025

💰 Late Fee: ₹200 per day

₹100 CGST

₹100 SGST

🔒 Maximum Late Fee Cap:

Limited to 0.25% or 0.5% of annual turnover in the respective State or UT, as applicable under GST law

Structural & Reporting Changes Introduced 🆕🧩

Several important changes affect how information is reported for FY 2024–25:

📂 Revised ITC Reporting

Table 6A1: ITC of earlier financial years claimed in the current year

Table 6A2: ITC pertaining strictly to the current financial year

🔄 GSTR-1A Auto-Population

Any supply additions or amendments made through GSTR-1A will now automatically reflect in the annual return

🛒 E-commerce Supply Disclosure

New reporting fields added for supplies made through e-commerce operators under Section 9(5) of the CGST Act

💳 Flexible Tax Liability Payment

Additional tax identified during reconciliation can be paid using cash or available ITC, offering more flexibility than earlier provisions

Filing & Authentication Requirements 🔐🖊️

🏢 Companies and LLPs:

Filing must be authenticated using a Digital Signature Certificate (DSC)

👤 Other Taxpayers:

May authenticate using Electronic Verification Code (EVC)

📘 Self-Certified Reconciliation

GSTR-9C is now self-certified, though it must be prepared using audited financial statements

Important Compliance Notes ⚖️📌

❌ No Revision Allowed

Once filed, GSTR-9 and GSTR-9C cannot be revised under any circumstances

📊 Accuracy is Critical

All disclosures must match audited records, returns filed during the year, and reconciliation data